What follows is a scenario, not a prediction.

The intent of this piece is to model a scenario that is relatively underexplored by academic administrators and leaders in higher-education. It was inspired by a scenario analysis published by Citrini Research, and it seeks to model how AI could reshape the higher-education landscape as it simultaneously reshapes the economy.

Hopefully, it will leave university leaders and boards more prepared for our inevitable future with AI.

Some of what it describes has already begun. Some has not. All of it could.

This is the Wilson Research briefing published on November 22, 2031, detailing the progression and fallout of the American Higher Education Crisis.

The Arithmetic of Collapse

21% gone. The composition is catastrophic.

The preliminary fall enrollment numbers arrived this morning. Total undergraduate enrollment across the United States: 12.8 million. A 21% decline from 2025. A 12% drop from just two years ago.

The composition is catastrophic. Non-elite private institutions have lost a third of their students since 2025. Regional public universities, the workhorses of the system, the places where most Americans actually go to college, are down 27%. Professional school enrollment has been cut nearly in half. The number of active Title IV degree-granting institutions in the United States, which stood at 3,896 in 20231, is on a trajectory toward 2,800 within the decade. More than 300 private nonprofit colleges have closed or announced imminent closure since 2025: a pace that began at one per month and ended at nearly two per week. Another 340 sit on what Moody's now calls "terminal financial watch," running deficits exceeding 10% of operating revenue with fewer than five years of reserves remaining.

The acceleration tells the story better than any single number:

| Year | Closures | Average rate | Cumulative (from 2025) |

|---|---|---|---|

| 2022 | 9 | — | — |

| 2023 | 14 | — | — |

| 2024 | 17 | — | — |

| 2025 | 16 | ~1 / 3 weeks | 16 |

| 2026 | 21 | ~1 / 2 weeks | 37 |

| 2027 | 40 | ~1 / week | 77 |

| 2028 | 59 | ~5 / month | 136 |

| 2029 | 78 | ~7 / month | 214 |

| 2030 | 86* | ~1.7 / week | 300 |

* 2030 figure annualized from Q1–Q3 data. Sources: National Student Clearinghouse, IPEDS, Moody's Investors Service. Pre-2025 figures reflect actual closures; 2026–2030 figures reflect scenario projections consistent with Moody's terminal watch designations.2

Two years ago, numbers like these would have been front-page news. Now they barely register. The country has grown numb. The closures blend together. The campus towns empty out quietly. The debt accumulates.

The mechanism is now clear. American higher education met its demographic cliff at the precise moment that artificial intelligence began dismantling the entry-level white-collar economy, and the two forces compounded. Demography alone would have produced an orderly contraction. It is what administrators and boards had prepared for. But what they did not model was the downstream effects of AI-related entry-level job losses. The job market that four-year college degrees had pointed to was collapsing, and with it, the willingness of students to debt-finance an expensive degree.

And the system that has organized American intellectual and economic life since the GI Bill continues to unravel, institution by institution, semester by semester, with the inevitability of a structure whose load-bearing walls have been removed.

This is how it happened.

A patient with a pre-existing condition.

The sector had known the cliff was coming and hadn't sufficiently prepared.

American higher education in 2025 was a patient with a pre-existing condition. Several, actually.

The demographic cliff had been forecast for over a decade. The number of 18-year-old high school graduates peaked at roughly 3.9 million in 2025 and then began the descent that the Western Interstate Commission for Higher Education had been warning about since the mid-2010s: a projected 9% decline in the high school graduate population between 2026 and 20313, with the steepest drops concentrated in the Midwest and Northeast. By 2041, Illinois was predicted to have 32% fewer graduates; California: 29%; New York: 27% fewer.4 Nathan Grawe, the Carleton College economist who had spent a decade modeling this, took no satisfaction in being right.

The sector had known the cliff was coming and hadn't sufficiently prepared. Instead, it had engaged in a decade-long arms race of competitive discounting. By the 2024–25 academic year, the average tuition discount rate at private nonprofit institutions had reached a record 56.3% for first-time, full-time undergraduates.5 Although the sticker price at a private college was $45,000 a year, the average student actually paid less than half. The schools were collecting roughly 44 cents on every dollar of listed tuition, and the most vulnerable ones far less. Net tuition revenue was still rising, barely, by about 1.4% in real terms. But the math only worked if enrollment held. Each incoming class was recruited at a deeper discount than the last, and the strategy depended entirely on a supply of students that demography had already promised to take away. It was a treadmill, and the belt was accelerating.

Already in 2024, more than half of private universities rated by S&P Global generated operating deficits.6 Student loan debt stood at $1.833 trillion across 42.8 million borrowers. Federal student loan delinquency had climbed over 10% by late 2025, with 20% of borrowers behind on payments. Over 100 colleges had closed or merged in the prior eight years.7 The share of high school graduates immediately enrolling in college had dropped from 70% to 62% over the prior decade.8 And in the final weeks of 2025, all three major credit rating agencies issued negative outlooks for the higher education sector in rapid succession: Moody's on November 21, S&P Global on December 3, and Fitch on December 5.9

Meanwhile, the employers on the receiving end of the pipeline were quietly dismantling the requirement that had funneled students into the system in the first place. By 2023, Google, Apple, IBM, Bank of America, Walmart, Accenture, and Delta had all dropped bachelor's degree requirements for significant categories of roles.10 By 2025, a quarter of employers surveyed planned to eliminate degree requirements for some positions by year's end, and 70% of hiring managers said they prioritized relevant experience over a diploma.11 The trend was still early, still unevenly applied, and still easy to dismiss as a tight-labor-market anomaly. But it revealed something the universities preferred not to examine: that the employers who had spent decades requiring bachelor degrees were discovering they didn't actually need them.

The 2024-2025 period showed the early signs of contraction. Birmingham-Southern College, which was 168 years old and once home to six Rhodes Scholars, had bled its endowment from $122 million to $26 million. Enrollment had collapsed from 1,500 to 731 before its final commencement.12 Sixteen more nonprofit institutions closed in 202513: Fontbonne University in St. Louis (founded 1923), Northland College in Wisconsin (founded 1892), Eastern Nazarene College near Boston, and Limestone University in South Carolina (which owed 281 students nearly $400,000 in refunds when the doors shut).14 Martin University, an HBCU in Indianapolis, paused operations in December 2025 and closed in January 202615 — early enough to be written off as an outlier, late enough to be recognized as a harbinger.

The question, even then, was no longer whether the system was contracting. It was whether the contraction would be orderly.

Penn State's board, meanwhile, approved the closure of seven of its nineteen Commonwealth Campuses, the satellite locations that had served as on-ramps to the Penn State degree.16 The board voted on the closures in the same session it reaffirmed the $700 million Beaver Stadium renovation. The brand would be preserved. The access mission would not.

Each followed the arc Hemingway described for bankruptcy: gradually, and then suddenly.

But in 2025 and early 2026, the closures were still understood as isolated failures: bad management, bad luck, niche institutions with niche problems. The system, everyone agreed, was under pressure. The system was not in crisis.

But the system was in crisis.

Computer science was the canary.

If AI could displace the most technically sophisticated graduates, it could displace anyone whose work was primarily cognitive.

By early 2026, the fracture was already visible in the 2025 data itself. When the National Student Clearinghouse released its final fall enrollment numbers in January, total undergraduate enrollment had recovered to 16.2 million, within 400,000 of the 2019 peak. The headline read as recovery. The composition read as warning. Community college enrollment rose 3.0%. Public four-year rose 1.4%. Private nonprofit four-year declined 1.6%. For-profit four-year declined 2.0%. The aggregate was climbing. The institutions most exposed to the coming storm were already contracting, inside what was otherwise a recovery year.

The first tremor that should have rewritten everyone's assumptions arrived in the fall of 2026, and almost nobody recognized it for what it was.

Computer science enrollment — the hottest major in American higher education for a decade, the field parents pushed their children toward, the degree that almost guaranteed an eventual six-figure salary — was declining.

Not at a handful of struggling schools. Across every institution type and award level. Undergraduate CS fell 3.6%. Graduate CS fell 14.0%.17

This was counterintuitive. AI was the most transformative technology since the internet. Surely the people who built AI tools would thrive? But the agentic AI systems that emerged in early 2026 (Claude Code, Codex, Cursor, and their successors) did not simply automate tasks. They restructured the economics of software development. A team of twenty became a team of five. Amazon shed 16,000 jobs in January. Dell cut 11,000 in March. Meta 8,000 in May. Even Microsoft was now offering voluntary retirement to 7% of its workforce. By fall 2026, the pattern was accelerating.

In the financial markets, the iShares Software ETF fell roughly 24%.

Challenger, Gray & Christmas reported in March of 2026 that AI was the single most-cited reason for layoffs in the United States, accounting for 25% of all job cuts that month. Technology alone shed 52,050 workers in Q1 2026, up 40% year-over-year. The man whose firm tracked the data put it plainly: "Companies are shifting budgets toward AI investments at the expense of jobs."18 But these early signs were often ignored or dismissed as the mere 'AI-whitewashing' of regular layoffs.

But for the parents of a high school junior watching these layoffs, the calculation changed overnight. If AI could write better code than most mid-level developers, what exactly were they buying for $200,000?

The establishment treated the CS enrollment dip the way Wall Street treated subprime mortgage defaults in early 2007: contained. A sector-specific correction. Technology adjusting to new tools. "Students are just recalibrating," a dean at a top engineering school told the Chronicle of Higher Education in February 2027. "The fundamentals of a CS education remain strong."

They didn't realize it was the canary. If AI could displace computer science graduates, which were the most technically sophisticated products the university system produced, it could also displace anyone whose work was primarily cognitive. And that was not a niche. That was the entire white-collar economy, which represented roughly 70% of the jobs university graduates had historically filled.

A friend of ours is a senior product manager at a mid-sized SaaS company in Dallas with a Baylor MBA and twelve years of experience. He was laid off in March 2027. His entire product team was restructured around AI tools. He spent four months applying for roles before accepting a position at 60% of his previous salary. "For twenty years the degree opened every door I needed," he said. "Now the doors are gone. I'm competing against agents that never sleep, never ask for raises, and keep getting smarter every week."

By the fall of 2027, the broader impact was technically measurable, but still easy to misread. Freshman enrollment at non-elite private institutions was down roughly 8% from 2025 levels. At regional publics, 6%. The numbers were bad, but within the range demography alone could explain, and administrators attributed them accordingly. Meanwhile, applications to the top 50 national universities increased. Harvard, Princeton, and Yale hit record numbers. The bifurcation had begun. Almost no one recognized it yet. The flight-to-quality that economist Richard Vedder had described for years went into overdrive.

AI was not eliminating careers. It was eliminating the entry point to careers.

The work didn't disappear. The bottom of the pyramid did.

The universities that saw what was coming did what universities always do: they launched new programs.

Lipscomb University in Nashville, TN went all in. By 2024, it had launched Nashville's first graduate program in applied AI — a Master of Science and certificate track designed to equip working professionals with AI fluency. In 2025 campus-wide enterprise AI access followed. An AI committee. An official usage policy. AI bots embedded in the education school's courses. Lipscomb's provost said what every provost was thinking: "Our mission is to prepare students for a world that doesn't yet fully exist."

The University of South Florida enrolled 3,000 students in a new AI and cybersecurity college. Columbia, USC, Northwestern, and the University at Buffalo all launched AI-specific degree programs. MIT's AI and Decision-Making major became the second-largest on campus. Across the country, universities were doing what the adaptation blueprint said they should: pivoting toward the technology, building curricula around it, positioning their graduates to ride the wave rather than be drowned by it.

It was the right response to the wrong question.

The programs were primarily built around "AI literacy," which is the ability to work productively with AI tools, to understand their capabilities and limitations, to integrate them into professional workflows. The question was whether this would be a durable, high-value skill that justified years of study and tens of thousands of dollars in tuition. For a narrow window, roughly from 2026 to 2029, it was. Employers wanted people who understood prompt engineering, model selection, retrieval-augmented generation, agentic workflows. The universities that moved fast captured that demand.

But AI literacy had the shelf life of a transitional skill, not a professional discipline. The analogy was not learning to practice medicine. The analogy was learning to type.

In 1985, community colleges across America offered typing courses. They were practical, vocational, and genuinely useful because most adults did not know how to use a keyboard. By 1995, every teenager in the country could type, because they had grown up with computers in their homes and schools. The skill was absorbed into the ambient competence of the population. The courses disappeared, not because typing stopped mattering, but because it stopped requiring formal instruction.

AI fluency followed the same trajectory, faster. A child who began using Claude or its successors at age thirteen grew up building projects with AI assistants. They learned to prompt naturally the way earlier generations learned to Google, and this new generation did not need a $160,000 degree to become "AI literate." They already were. By 2029, most high schools had absorbed AI tools into everyday coursework the way they'd once absorbed graphing calculators. AI was no longer a subject to study but infrastructure to use. Students were using AI to research, write, and work through problem sets before they'd filled out a college application. By 2030, the first cohort of AI natives were entering the workforce without having taken a single college course in applied AI. They didn't need to. Asking them to pay for AI literacy training was like asking a native English speaker to pay for English lessons.

For older workers retraining mid-career, the value of structured AI education lasted somewhat longer. But even here, the economics were fatal to the university model. An eight-week bootcamp, a $500 online certificate, or a corporate training program could all deliver AI fluency at a fraction of the cost of a graduate degree, on a timeline that matched the urgency of career transition. The market for AI upskilling was real, but it was a market for speed and affordability, not for the slow, expensive, credit-hour-denominated education that universities were structurally designed to provide.

The deeper problem, though, was not that universities were teaching the wrong skill. It was that they were training students for a labor market whose entry points were being eliminated.

On March 13, 2026, at Palantir's AIPCON conference, company architect Chad Wahlquist described the transformation of military intelligence targeting using the Maven Smart System. Work that once required roughly 2,000 intelligence officers (identifying targets, analyzing data, developing courses of action) now required about 20, and they were doing it faster.19

The ratio was not a prediction. It was an operational fact, reported during an active U.S. military campaign. In that same month, job postings for entry-level roles on Handshake had fallen 16% compared to the prior year, while applications per role surged 26%.20 Fifty-eight percent of 2024 and 2025 college graduates were still looking for their first job.21

By early 2029, that ratio — not the specific number, but the structure of labor compression — was repeating across every white-collar field the university system fed. The entry-level financial analyst who built models in Excel: replaced by a senior analyst with a team of AI agents. The junior associate who spent two years doing document review: replaced by a platform. The first-year management consultant who assembled slide decks from data: redundant. The entry-level marketing coordinator who wrote copy and managed campaigns: automated.22

Although no corporate setting had replicated Maven's 100:1 compression, ratios of 5:1 and 10:1 were becoming routine. A McKinsey engagement that once staffed eight analysts and two partners now staffed two analysts and two partners. A mid-size accounting firm that once hired twelve first-year associates hired three. In each case, the senior people survived. They had judgment, relationships, institutional knowledge, and the capacity to evaluate AI output rather than merely produce it. The work itself didn't disappear. The bottom of the pyramid did.

This was the mechanism that university administrators, board members, and parents needed to understand, and for a time almost no one was getting it. AI was not eliminating careers; it was eliminating the entry point to careers.

You do not become a senior intelligence analyst without first being a junior one. You do not become a partner at a law firm without first being a junior associate. You do not become a CFO without first being a financial analyst. The entire structure of professional advancement in the white-collar economy was built on an apprenticeship model: you entered at the bottom, learned on the job, developed judgment through repetition and mentorship, and rose. AI collapsed the bottom. It removed the first rung of the ladder. And for millions of families, the university degree was the ticket to that first rung. When the rung started disappearing, the ticket became worth a lot less. Not because it was a bad ticket, but because there were now fewer places to step.

The universities that had rushed to build AI programs early in the cycle were thus solving for both the wrong skill and the wrong destination simultaneously. They were teaching AI literacy, a skill that would be ambient within a generation, to prepare students for entry-level cognitive work, a category that was being structurally eliminated.

The adaptation was real. It was also too late.

The cross-subsidy was the load-bearing wall, and it collapsed.

Law, business, accounting — the profit centers that quietly carried the rest of the university.

This headline, when it landed, should have ended the debate. It didn't, because by October 2028 there were too many crises to track. But it mattered more than almost anything else that happened that year, because of what it revealed about the internal economics of universities.

Professional schools (law, business, accounting) were not just programs. They were profit centers that charged higher tuition and offered lower discount rates to generate the surplus revenue needed to sustain the rest of the university ecosystem. When these programs shifted from surplus-generating to running deficits, the entire university budget came under simultaneous pressure. There was no reserve. There was no buffer. The cross-subsidy had been the load-bearing wall, and it collapsed.

Law school, with exquisite irony, had been booming. LSAC data showed applicants up 18% for the 2025 cycle23 and 33% year-over-year in early 2026 data.24 First-time LSAT takers surged: up 18% in August, 24% in September, and 16% in October.25 Mike Spivey, a veteran admissions consultant, said he had never seen a cycle start so strong in 26 years of watching the data.26 The reasons were familiar: when the economy frightens people, they flee to professional school. It was shelter-seeking behavior. The 2008 script, run again.

But it wasn't shelter. It was a trap. The signals that law school deans and the general public weren't paying attention were found in the VC markets. Legal AI investment topped $5 billion in 202527 and another $10 billion by the end of 2026. Startups like Legora had raised $800 million in a matter of 10 months.28 In May of 2026, Anthropic announced Claude Legal Solutions, which gave lawyers native Claude integrations into 20 software platforms across 12 different practice types.29

By 2028, AI tools could perform document review, contract analysis, due diligence, and regulatory compliance at a level that had required teams of junior associates billing $400 an hour. Large firms flattened their pyramids. Regional firms discovered that a solo attorney with an AI subscription could handle a caseload that previously required three associates and a paralegal. The class of 2028 graduated $150,000 to $250,000 in debt into a market that no longer valued what they'd purchased. The application surge of 2026 became, by 2029, a violent reversal. At least a dozen law schools closed or announced closure. Another thirty operated below sustainable enrollment.

A young woman we know in the top 15% of her class at a well-regarded (but not top-14) law school had her offer rescinded two weeks before her May 2029 start date. The firm had adopted an AI contract review platform and didn't need the associate class it had planned. She had $210,000 in debt. She took a compliance role at a bank at roughly half the salary she'd expected. "I did everything right," she told a mutual friend. "Every single thing they told me to do. And it didn't matter."

Accounting was hit even harder. The Big Four had been quietly reducing entry-level hiring since 2025, as AI automated audit procedures, tax preparation, and advisory analysis. PwC deployed an internal AI platform that could complete a standard audit workpaper in minutes rather than the hours it took a first-year associate. By 2028, Deloitte's campus recruiting events, which were once the lifeblood of accounting programs at mid-tier universities, had been cut by two-thirds. Accounting majors at programs outside the top 25 saw placement rates fall below 50%. The CPA pipeline crisis the AICPA had worried about for years was solved: the need for the pipeline was eliminated.

The MBA followed. Two-thirds of less selective programs had already reported declining applications in 202530, before AI became the primary narrative. Corporate middle management, the layer that MBA programs existed to feed, was being hollowed out, and the value proposition of a $180,000 MBA outside the top 20 simply ceased to exist.

There was nothing left to cross-subsidize with.

The administration dismantled the architecture and promoted its replacement.

A humanoid robot on the East Room red carpet, while Grad PLUS quietly disappeared.

On March 25, 2026, the First Lady of the United States walked a red carpet in the East Room of the White House alongside a humanoid robot. The machine, produced by the California startup Figure AI and designated Figure 03, introduced itself to an audience of foreign dignitaries' spouses in eleven languages. Melania Trump then asked the room to imagine a humanoid educator named "Plato." Plato would be patient, always available, and able to deliver personalized instruction in literature, science, philosophy, and mathematics in the comfort of a family's home. Education Secretary Linda McMahon smiled from the front row.31 The American Federation of Teachers called it "every parent's nightmare." The administration called it the future.

It was not an isolated stunt. It was the policy signal, delivered in the most literal terms imaginable. The same administration that was dismantling the financial architecture of American higher education was simultaneously promoting the technology that would replace the human instruction universities provided. The message could not have been clearer if it had been printed on the robot's chassis.

And even if the robots were not ready yet, the substitute teacher was not hypothetical. In April 2025, Anthropic had launched Claude for Education with campus-wide partnerships at Northeastern (50,000 students across thirteen campuses), the London School of Economics, and Champlain College, shipping a "Learning Mode" feature that guided student reasoning rather than supplying answers. Plato the robot was a proposal, but the Socratic teaching he was meant to deliver was already a product.32

The Trump administration's proposed budget was the substance behind the signal. Its FY2026 budget proposed cutting NIH by nearly $18 billion and NSF by $5.1 billion, representing roughly 40% and 57% reductions since FY2024.33 By mid-2025, the administration had targeted $3.3 to $3.7 billion in university grants for termination, affecting more than two-thirds of land-grant universities and nearly half of HBCUs.34 The University of Chicago paused PhD admissions in sixteen or more humanities and social science departments.35 Northwestern cut over 400 staff positions. The UC system warned that federal cuts would cost $4 to $5 billion per year to replace. UT Austin began consolidating and closing departments, including American Studies, in early 2026.36

Simultaneously, the One Big Beautiful Bill Act restructured the student loan apparatus more dramatically than anything since the Higher Education Act of 1965. It eliminated Grad PLUS loans, replacing them with capped annual limits: $20,500 for graduate students, $50,000 for professional students. It terminated most income-driven repayment plans for new borrowers. And it introduced an Earnings Premium metric tying program eligibility for federal aid to graduates' post-graduation earnings.

The Earnings Premium was long-overdue accountability: tying program eligibility for federal student loans to what graduates actually earned. But it began biting in the summer of 2028,37 precisely when AI was depressing wages across every white-collar field the metric measured. The metric couldn't distinguish between a bad program and a disrupted economy. Programs in business, IT, communications, and engineering at lower-ranked institutions began shrinking, and the loan eligibility that their students depended on started disappearing.

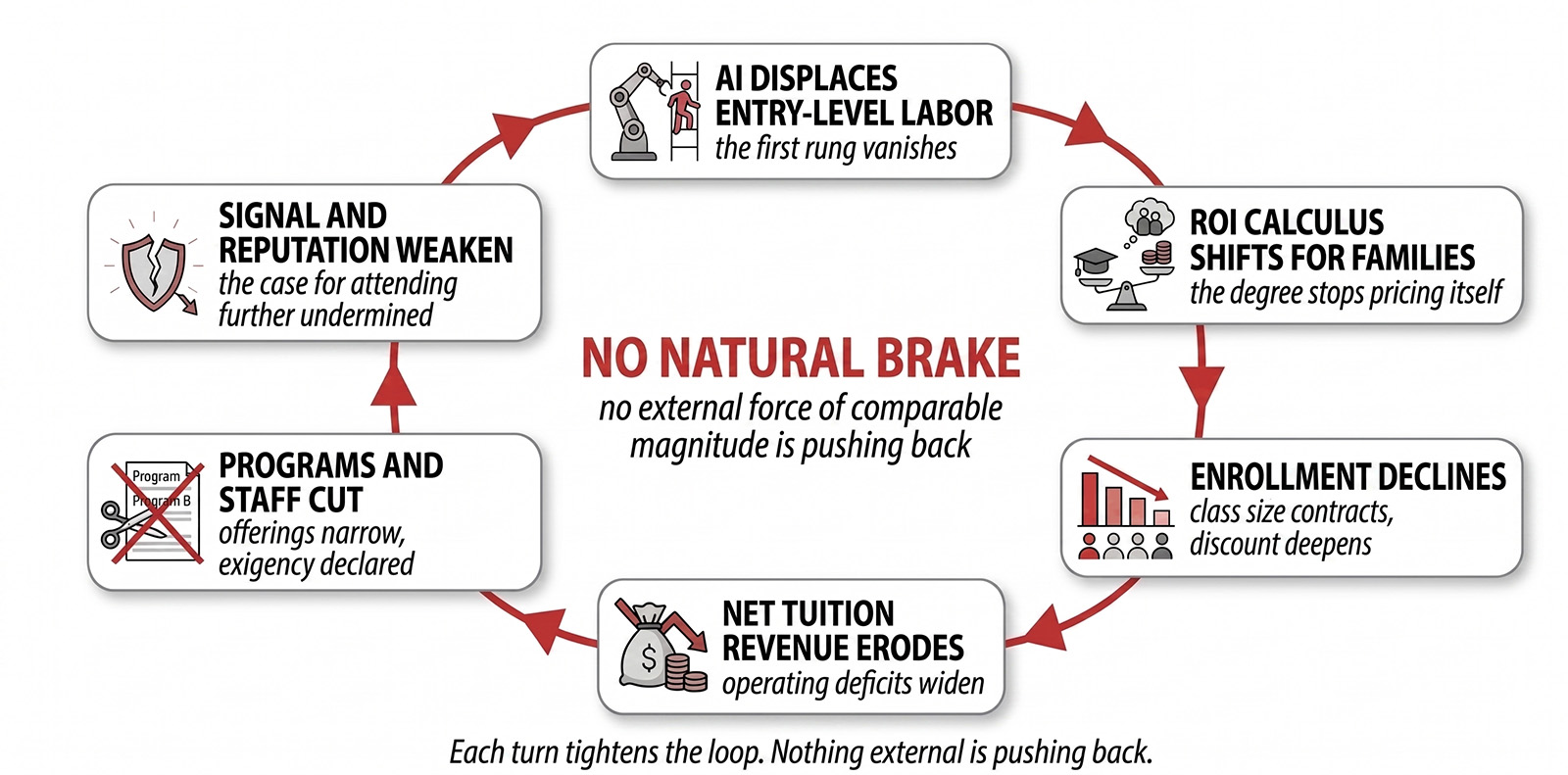

The loop had no natural brake.

Four crises — demographic, technological, financial, regulatory — fused into a single self-reinforcing feedback loop.

By the fall of 2028, the individual crises (demographic, technological, financial, regulatory) had fused into a single self-reinforcing feedback loop. AI displaced white-collar workers. The entry-level positions that justified expensive degrees were evaporating. Students stopped enrolling. Universities lost revenue. They cut programs and staff, narrowing what they could offer, further undermining the case for attendance. To sustain enrollment they discounted deeper, which eroded net tuition revenue further. More closures followed. Each closure shook confidence in the system.

The loop had no natural brake.

In 2029, the broader economy entered what analysts would call the Intelligence Recession. It was a downturn driven not by a financial bubble or external shock but by the structural devaluation of human cognitive labor. AI capabilities had continued their exponential climb. By mid-2028, the leading models could perform essentially any computer-based cognitive task at human level or above. AI models could completely run desktop computers, like a human could, and AI-powered robotics were becoming an increasingly normal part of manufacturing and distribution. Dario Amodei had warned publicly since 2025 that AI could eliminate half of entry-level white-collar jobs and spike unemployment to 20%.38 Sam Altman had funded the largest basic income study in American history and advocated for wealth redistribution as AI reshaped the economy.39 The warnings were on the record. The preparation was not.

Unemployment climbed past 7%, then 8%. The composition was unprecedented: the hardest-hit cohort was college-educated workers between 25 and 45, the demographic historically most insulated from recessions. The "Salesforce PM to Uber driver" trajectory that had been a dark joke in 2027 was becoming a statistical reality. The only problem was that autonomous vehicles were now closing even that escape valve. The equity markets reflected the bifurcation: AI infrastructure companies posted record revenues, but the equal-weighted S&P 500 fell far more steeply than the cap-weighted index. Consumer discretionary stocks cratered. Regional banks with heavy commercial real estate exposure came under severe strain as office vacancy rates spiked. If AI was replacing the white-collar workers, who needed the office space?

For higher education, the Intelligence Recession was a structural collapse layered on top of a contraction already in progress.

A parent in our community, whose daughter was a high school junior in 2028 (strong student, exactly the kind of kid who five years earlier would have been headed to a selective private university), described the dinner-table conversation where the family decided against a four-year degree. "We looked at what happened to her cousin," the mother said. "Rose-Hulman, engineering degree, $80,000 in debt, laid off eighteen months after graduation. We couldn't do that to her. She's at the community college. She's going to be a dental hygienist."

That conversation, multiplied by millions of families, was the crisis in miniature.

State funding collapsed in parallel. The states where AI displacement hit hardest (California, New York, New Jersey, Connecticut, and Massachusetts) were the same ones with the most income-tax-dependent budgets. Cal State, the largest four-year public system in the nation, closed three campuses and converted two more to community college status.

The privates fell faster. By the end of 2029, closures were running at roughly seven per month. The Philadelphia Fed's 2024 prediction of 80 closures per year, which modeled demographic decline only and did not account for AI-driven labor market disruption, was no longer the worst-case. It was the demographic baseline. The AI shock was on top of it. The early closures had been small, fragile institutions: Siena Heights,40 Lourdes,41 and Clarks Summit,42 all schools already on the edge. By 2029, the failures had moved up the food chain, reaching institutions with enrollments of 3,000 to 5,000. Endowments that had seemed adequate five years earlier were no longer adequate, and alumni networks couldn't believe what was happening.

The federal response, when it finally arrived, was not designed for universities. In early 2030, the American Council on Education mounted the most aggressive lobbying campaign in its history, seeking emergency stabilization funding modeled on the direct institutional relief Congress had provided during COVID.

The pitch was familiar: universities were community anchors, research engines, employers of 3.5 million people. Congress was sympathetic in language and immovable in practice. The emergency workforce legislation that passed in the summer of 2030 created retraining vouchers, expanded community college funding, and established portable benefit accounts for displaced workers. Every dollar was aimed at individuals.43 Not a single provision was directed at sustaining four-year colleges or universities. The political constituency for "save my job" had overwhelmed the one chanting "save my alma mater."

The electrician outearned the CS graduate. The plumber outlasted the paralegal.

The hierarchy that had organized American economic life for half a century partially inverted.

By 2030, the hierarchy that had organized American economic life for half a century had partially inverted. A licensed electrician with a two-year certificate earned more, with greater job security, than a CS graduate from a non-elite university. A plumber was more insulated from disruption than a paralegal. A nurse practitioner had better career prospects than an MBA from a school ranked outside the top 20.

Community colleges experienced a genuine renaissance. As four-year degrees lost their signaling value, demand surged for credentials that led to work AI could not do. Enrollment at public two-year institutions rose roughly 12% between 2027 and 2030, even as four-year enrollment cratered.

The student debt crisis became grotesque. The 2025 $1.833 trillion in outstanding loans had grown to over $2 trillion. Delinquency, which had stood at 10% in late 2025, climbed past 27%. Debt had accumulated under the assumption that the degrees would produce the incomes necessary to service them. But for millions of borrowers, that assumption was collapsing. The chilling effect on future enrollment was worse than the defaults themselves. By 2029, every parent and high school senior could see the stories. The cost-benefit analysis, which had been the university's strongest recruiting tool for decades, now worked against it.

The diploma that had functioned as an economic signal was breaking. Not because employers found a faster way to screen candidates, but because the jobs the screening fed into were disappearing. The remaining human roles, the ones that survived the compression, were more valuable, not less.

Managing a team of AI agents that replaced twenty analysts required judgment, institutional knowledge, the ability to evaluate machine output against real-world context. These were high-trust positions, and companies filled them the way high-trust positions have always been filled: through networks, referrals, demonstrated track records, extended evaluation. A senior partner didn't hire her AI operations lead based on a diploma. She hired someone she'd watched work for three years. The process was slower, more deliberate, more relational. The opposite of mass credentialing.

The university had spent decades as the sorting mechanism for the American labor market: the place where millions of undifferentiated 18-year-olds were processed into ranked, credentialed workers for employers who needed a shortcut for evaluating strangers. AI didn't eliminate that function. It eliminated the need to hire strangers.

And beneath the economics festered a deeper wound. The university had been the central institution of the American meritocracy: the place where intelligence was cultivated and converted it into social status. When society collectively realized that cognitive ability could be replicated by a machine for pennies, the university did not just lose its market. It lost its meaning. The wound was not economic. It was existential: the thing you trained your whole life to do no longer had value. And it made the next enrollment cycle worse, because the despair felt by parents was visible to every 18-year-old deciding whether college was worth it.

The institutions that needed to change least were most capable of changing.

What survived told us what a university actually was, once the vocational scaffolding was stripped away.

By summer of 2030, the landscape had resolved into a brutal clarity. What survived told us what a university actually was, once the vocational scaffolding was stripped away.

The elite research universities survived and consolidated power. Harvard's $50 billion endowment could sustain the institution indefinitely with zero tuition revenue. Stanford, MIT, Princeton, and their peers were insulated by endowments, brand equity, and the self-reinforcing logic of elite credentialing: the more chaotic the economy, the more desperately families sought the safety of a name-brand degree. Acceptance rates, already below 4%, fell below 2%. These were less universities than luxury brands with research operations attached, and the crisis widened the moat. MIT restructured around AI-human collaboration. Stanford launched an AI Residency program. They had the resources to experiment and the brand to attract students regardless. The irony was thick: the institutions that needed to change the least were the ones most capable of changing. The ones that needed radical reinvention had no resources to attempt it.

Universities with genuine research capacity in fields essential to the AI buildout (materials science, power systems, semiconductor design, the mathematics of machine learning) found new funding models. Corporate money partially replaced declining federal support, though it came with strings that made faculty uncomfortable and raised legitimate questions about intellectual independence. The institutions that navigated this were ones with something the private sector couldn't easily replicate: deep expertise, long time horizons, willingness to pursue work that might not pay off for a decade. Georgia Tech, Purdue, and the University of Michigan were schools with strong engineering programs and established industry relationships. They found leverage they hadn't anticipated.

A handful of small institutions survived by being genuinely, irreplaceably distinctive. Hillsdale College, with its refusal of all federal funding since the 1980s and its unflinching commitment to the classical liberal arts. St. John's College, with its Great Books curriculum that had never pretended to be vocational in the first place. A few others. Their survival proved a thesis: that there is a market for education understood as formation rather than credentialing. But it simultaneously was proving how small that market is.

Community colleges and trade programs were the smartest bet in higher education. Low tuition, flexible scheduling, vocational credentials leading to work AI could not do.

Everything else was in trouble.

The story is not the closures. It is what is happening to the middle two thousand.

The large publics, the mid-tier privates, the regional comprehensives: restructured under financial duress, and still early.

The rate of closures since 2028 has commanded the headlines. But the closures are not the story. The story is what is happening right now at the two thousand institutions between Harvard and Northland College: the large public flagships, the mid-tier privates, the regional comprehensives with endowments of $500 million to $5 billion and enrollments of 10,000 to 40,000. These schools are not closing. They are being restructured under financial duress, and the process is still in its early stages.

For most of the decade, restructuring was easier to describe than to execute. The barrier was the accreditation regime, designed as both quality assurance and gatekeeping. In normal times the accreditation moat was an asset. In a disruption it became a prison. The standards required faculty-to-student ratios, physical plant, library resources, and governance structures designed for the model AI was making obsolete. Any institution that tried to restructure around AI from the bottom up triggered accreditation review, and review threatened Title IV eligibility, and that threatened survival. So the schools did what the rules permitted. They bought the AI tools and layered them on top of unchanged cost structures, paying for both models at once. Institutions that might have reinvented themselves died inside the framework, maintaining their faculty ratios and governance documents all the way to the closing ceremony.

The schools that survived did not break through the regulatory lock. They went around it. The enabling mechanism is financial exigency. AAUP guidelines permit the termination of tenured faculty when an institution faces genuine financial crisis. For decades, boards treated the provision as unthinkable. Then a few invoked it and survived the legal challenges. Then more followed. By the 2030–31 academic year, exigency declarations were no longer news.

At most universities, 60 to 70 percent of the operating budget is personnel, and tenure renders a significant portion of that a fixed cost. You cannot restructure a cost base you cannot touch. Until you can.

What follows exigency is amputation. We have watched entire departments being consolidated or eliminated. Programs whose graduates no longer have a labor market to enter are cut. Programs connected to licensing requirements and physical human presence, nursing, allied health, skilled technical fields, are expanded. The institution retains its name, its campus, its Saturday football games. It loses much of its previous academic character.

Tuition appears to be the primary dividing line for how fast the restructuring hits. Large public flagships charging $12,000 to $18,000 for in-state students have so far been buffered by both price and political protection. The governors of Indiana and Ohio have publicly declared they will not allow their flagship state institutions to fail, and we expect similar commitments from other states as the pressure builds. But state budgets are themselves under severe strain as the broader labor market contraction erodes income and sales tax revenue, and the protection of flagships will likely come at a cost. Regional campuses are increasingly sacrificed to preserve flagship institutions, a pattern Penn State set in 2025 when it closed seven satellite campuses while renovating its stadium. Community colleges will continue to be funded because they are the retraining vehicles that workforce legislation requires.

But everything between those two poles (the mid-tier privates, the regional comprehensives, the small denominational colleges with endowments under $500 million) will continue to occupy a political no-man's-land: too expensive to bail out, too numerous to save individually, and too far from the retraining mission to benefit from workforce funding. Within this exposed middle, then, the picture is uneven. Even the strongest privates in this band, the schools charging $50,000 to $65,000 with substantial endowments and loyal alumni, are showing price sensitivity that brand equity can no longer absorb. Donor engagement has been a meaningful buffer: at several institutions, major gifts have sustained programs and athletic departments through the worst of the transition. But donor capital follows sentiment, and as the restructuring reshapes the institutions donors remember, we are watching those commitments closely.

Some institutions in the middle have found real, if limited, savings by turning AI inward: financial aid processing, enrollment management, compliance reporting, student services. Administrative headcount reductions of 20 to 30 percent, achieved without touching a single faculty line, are buying time.

But efficiency gains are deferring the harder question, and the crisis is already answering it: distinguishing formation-as-marketing-copy from formation-as-institutional-commitment. Every university mission statement in America claims to develop critical thinking, ethical reasoning, and the capacity for lifelong learning. For most, that language has been decorative, wrapped around a fundamentally vocational product. A handful of institutions have meant it, building robust core curricula, investing in mentorship, sustaining communities that were real and not merely brochure copy. But the crisis is stripping the decoration away. What remains will either be a genuine institutional commitment to the cultivation of persons, or nothing.

Our expectation is not that the vast middle will vanish. But what emerges from this decade will be smaller, leaner, vocationally narrower, and unrecognizable to anyone who attended these institutions a generation ago. Whether that constitutes survival depends entirely on what you think a university is for.

The bargain is over, and nothing has emerged to replace it.

The future of the university may look much like its past.

The university, at its origin, was not a job-training program. The medieval university was founded on the conviction that the pursuit of truth was itself a worthy human activity; not because it produced economic returns but because it was constitutive of human flourishing. For a few centuries, the American university managed to serve both masters: it cultivated minds and prepared workers. The current crisis is fundamentally severing those two functions. AI has taken the second. The question is whether the first can survive without it.

What remains, when the vocational scaffolding falls away, is something closer to what higher education was before the GI Bill transformed it into a mass industry: a place for the cultivation of persons. A place where young people encounter ideas that challenge assumptions, form communities that shape character, and confront questions like, "What is a good life? What do I owe others? What is my purpose?" These are questions that artificial intelligence cannot answer. They are not questions about information, but about formation.

That probably sounds like a luxury for the wealthy. The truth is, without massive reinvention, it is. The First Lady had already named the replacement. She called it Plato.

The pre-industrial university with faculty-to-student tutoring was a preserve of the elite. The post-AI university may revert to something similar. The great democratic experiment of mass higher education was founded on the idea that a rigorous education should be available to anyone with talent and desire. This may turn out to have been a historical anomaly, enabled by a specific set of economic conditions that AI is now dismantling.

It is possible to imagine a future in which AI-augmented education is radically cheaper and more accessible, in which the cost barriers fall along with the vocational justification. It is possible to imagine institutions that reinvent themselves not as credentialing factories but as communities of inquiry oriented toward human flourishing. AI 'faculty' could be used for content delivery while human faculty focus on mentorship, dialogue, and the friction of one mind against another.

But imagining that future and building it are different things. The accreditation system resists it. The financial models don't support it. The political will does not exist. And the institutions best positioned to attempt it are the ones that don't need to.

The $700 billion education system as it has existed since the mid-twentieth century was built on a bargain. Families paid. Institutions credentialed. Employers hired. Each party's participation depended on the others, and for three generations the cycle held. AI has broken the employer's side of that bargain, and without it, the other two cannot sustain themselves. The universities will not all close. But the bargain that made them a mass industry is over, and so far nothing has emerged to take their place.

But you're not reading this in November 2031. You're reading it in May 2026.

The enrollment cliff hasn't fully hit. The professional school collapse hasn't arrived. The campuses haven't emptied. The cascade described in these pages is not history. It is a trajectory, however: a set of forces already in motion, accelerating, with no countervailing force of comparable magnitude. Larry Fink (CEO of BlackRock) told an audience last month that the class of 2026 may face the highest graduate unemployment in years, even without a recession. ServiceNow's CEO predicted in the range of 30%.44 The signals are not subtle.

The strongest objection to this scenario is not about policy or funding. It is about culture. The decision to attend college is not always a rational economic calculation for families. It is identity, aspiration, community expectation, parental hope. That cultural momentum has survived every previous challenge to the value of a degree, and it would be foolish to assume it breaks cleanly or quickly. In the Rust Belt, when manufacturing collapsed, families doubled down on education. The instinct to seek shelter in school is deep, and it will sustain enrollment longer than a pure economic model would predict.

But there is a difference between a slow erosion and a visible collapse. Manufacturing jobs disappeared from towns over decades, and the cause was diffuse enough that families could tell themselves education was the answer. The current displacement is happening in offices, on screens, to people with degrees, and it will be visible to every family with a group chat and a LinkedIn feed.

The cousin who was laid off eighteen months after graduation. The neighbor's son who can't find an entry-level role. The news that firms are rescinding offers. These are not abstract labor statistics. They are dinner-table conversations. And in this scenario, they happen at a pace that prior disruptions did not.

Cultural inertia is real. It will slow the decline. It will not stop it. The question is whether it slows it enough to give institutions time to adapt — and whether institutions use that time or waste it.

In this scenario, 21% is not the floor. It is the slope. Every indicator — demographics, labor markets, AI capabilities, federal policy, state budgets — points downward. The system that once held nearly 4,000 institutions could end up being down by a third. The question for every university president, every board member, every donor, and every alumnus is whether their institution is positioned to survive a disruption of this scale and speed.

The decisions that will determine that outcome are being made right now.

There is still time. Not much. But some.

What matters is what you do with it.

Source Notes

The following notes document the factual claims grounded in 2024–2026 data that underpin the scenario projections. All forward-looking elements (2027–2031) are scenario projections, not claims of fact.

- NCES Digest of Education Statistics, Table 317.10, prepared January 2024. https://nces.ed.gov/programs/digest/d23/tables/dt23_317.10.asp ↩

- In April 2026, the Huron Consulting Group projected that 442 of the nation's roughly 1,700 private nonprofit colleges were at significant risk of closing or merging within the decade. We think that number is conservative. As quoted in: Douglas Belkin, "The Small Private Colleges Dying in a Winner-Take-All University Marketplace," Wall Street Journal, April 8, 2026. ↩

- Western Interstate Commission for Higher Education (WICHE), Knocking at the College Door projections. Cited in CCCU, "Reality Check," Advance magazine: "between 2026 and 2031, WICHE projects a 9 percent drop (from 3.47 million graduates to 3.25 million)." https://www.cccu.org/magazine/reality-check/ ↩

- WICHE demographic projections for state-level high school graduate declines. These figures (Illinois 32%, California 29%, New York 27% by 2041) are from the WICHE Knocking at the College Door report series. ↩

- National Association of College and University Business Officers (NACUBO), 2024–25 Tuition Discounting Study. The 56.3% figure was widely reported across higher education media. ↩

- S&P Global Ratings, higher education sector outlook, 2024–2025. Referenced in multiple higher education publications and confirmed by the simultaneous negative outlook issuance in January 2026. ↩

- The College Fix, "16 colleges closed in 2025 and more could shut down in 2026" (January 14, 2026): "Over the past eight years, more than 100 colleges have closed or merged." https://www.thecollegefix.com/16-colleges-closed-in-2025-and-more-could-shut-down-in-2026/ ↩

- Education Next, "Colleges Are Closing. Who Might Be Next?" (November 25, 2025): "the share of high-school graduates enrolling in college right away has already shrunk from 70 percent to 62 percent over the last decade." https://www.educationnext.org/colleges-are-closing-who-might-be-next-how-machine-learning-fill-data-gaps-forecast-future/ ↩

- Moody's Ratings, "Higher Education Outlook 2026" (November 21, 2025), cited in Inside Higher Ed, "Moody's Projects a Negative Outlook for Higher Education" (November 25, 2025), https://www.insidehighered.com/news/business/financial-health/2025/11/25/moodys-projects-negative-outlook-higher-education; S&P Global Ratings, "U.S. Not-For-Profit Higher Education Outlook 2026" (December 2, 2025), cited in Higher Ed Dive, "S&P: Negative outlook for nonprofit colleges in 2026" (December 3, 2025), https://www.highereddive.com/news/sp-negative-outlook-nonprofit-colleges-2026/806983/; Fitch Ratings, "U.S. Higher Education Outlook 2026" (December 5, 2025), cited in Higher Ed Dive, "Higher education faces 'deteriorating' 2026 outlook, Fitch says" (December 5, 2025), https://www.highereddive.com/news/higher-education-faces-deteriorating-2026-outlook-fitch-says/807222/. See also Duke Chronicle, "'Big Three' credit agencies warn of negative outlook for higher education" (December 10, 2025), https://dukechronicle.com/article/duke-university-higher-education-sees-unfavorable-financial-outlook-three-credit-rating-agencies-20251210 ↩

- Glassdoor, CNBC, and company announcements, 2017–2023. Google, Apple, IBM, Bank of America, Walmart, Accenture, Delta, GM, Dell, and others dropped bachelor's degree requirements for significant categories of roles. See Computerworld, "Companies move to drop college degree requirements for new hires, focus on skills," August 2022. https://www.computerworld.com/article/1612670/companies-move-to-drop-college-degree-requirements-for-new-hires-focus-on-skills.html — See also CNBC, "Walmart is at work on a new degree-free message about getting hired at its corporate headquarters," November 2023. https://www.cnbc.com/2023/11/01/walmart-sends-a-new-degree-free-message-about-getting-a-corporate-job.html ↩

- Resume Templates survey of 1,000 hiring managers, May 2025, reported in Higher Ed Dive, May 29, 2025. Twenty-five percent of employers planned to eliminate degree requirements by year's end. Seventy percent of hiring managers prioritized relevant experience over a diploma. Eighty-four percent of companies that had already removed degree requirements reported the change as successful. https://www.highereddive.com/news/employer-eliminate-degree-requirements-2025/749061/ ↩

- Inside Higher Ed, "Birmingham-Southern announces abrupt closure" (March 27, 2024): "enrollment has slipped from more than 1,500 students in fall 2010…to 731 last fall." Endowment decline and financial details from Bhamwiki and Birmingham reporting. https://www.insidehighered.com/news/business/financial-health/2024/03/27/birmingham-southern-announces-abrupt-closure; see also https://www.bhamwiki.com/w/Closure_of_Birmingham-Southern_College ↩

- Inside Higher Ed, "The Colleges That Couldn't Survive 2025" (December 18, 2025): "At least 16 nonprofit institutions announced closures this year." https://www.insidehighered.com/news/business/mergers-collaboration/2025/12/18/colleges-couldnt-survive-2025; The College Fix corroborates: https://www.thecollegefix.com/16-colleges-closed-in-2025-and-more-could-shut-down-in-2026/ ↩

- Inside Higher Ed on Limestone University: "left its roughly 1,600 students in the lurch when they announced a sudden closure in May after a last-ditch $6 million fundraising effort failed." Fontbonne, Northland, and Eastern Nazarene details from same source and 2aDays compilation. https://www.insidehighered.com/news/business/mergers-collaboration/2025/12/18/colleges-couldnt-survive-2025; https://www.2adays.com/blog/college-shutdown-surge-update-the-full-list-of-2025-closures-and-mergers/ ↩

- Bryan Alexander, "Campus cuts, closures, mergers, and layoffs for winter 2025–2026" (February 2026): "Martin University (Historically Black University, Indiana) 'paused operations' in early December, then let all staff go a couple of weeks later, then announced it would close in January." https://bryanalexander.org/horizon-scanning/campus-cuts-closures-mergers-and-layoffs-for-winter-2025-2026/ ↩

- Inside Higher Ed, "The Colleges That Couldn't Survive 2025" (December 18, 2025): "Penn State's Board of Trustees signed off on a controversial plan in May to close seven of 19 Commonwealth Campuses…Collectively, they enrolled almost 3,200 students." The $700M stadium renovation context from same article: "it comes at a time the university is investing hundreds of millions into athletics at the flagship campus, including a $700 million stadium renovation." https://www.insidehighered.com/news/business/mergers-collaboration/2025/12/18/colleges-couldnt-survive-2025 ↩

- National Student Clearinghouse Research Center, Final Fall Enrollment Trends (January 15, 2026): Enrollment in Computer and Information Science programs declined across all award and institution types in fall 2025, ranging from −3.6% at undergraduate degree-granting institutions to −14.0% at the graduate level, the steepest single-year field-specific contraction in the release. https://nscresearchcenter.org/final-fall-enrollment-trends/. See also CRA CERP Pulse Survey (October 2025). Primary data on the 2025 decline and context for why it may persist (labor market / AI concerns, international enrollment shifts): https://cra.org/crn/2025/10/cerp-pulse-survey-a-snapshot-of-2025-undergraduate-computing-enrollment-patterns/. See also Encoura report, "From Surge to Shift: The Enrollment Crossroads for Computer Science" (April 2026), which explicitly flags "further declines ahead" via Eduventures funnel data: https://www.encoura.org/resources/wake-up-call/from-surge-to-shift-the-enrollment-crossroads-for-computer-science/ ↩

- Challenger, Gray & Christmas AI-attributed job cut data and technology sector layoff figures from early 2026 reporting. Workday and Amazon corporate layoff figures from company announcements widely covered in financial media. iShares Software ETF (IGV) performance from market data. ↩

- Palantir AIPCON conference, March 13, 2026. Company architect Chad Wahlquist described the Maven Smart System's transformation of military intelligence targeting, reducing the personnel required from roughly 2,000 intelligence officers to approximately 20. Video of the presentation is available via Palantir's official channel. ↩

- Handshake, early-career talent platform data reported in Fortune, March 18, 2026: job postings for early-career roles fell more than 16% between August 2024 and August 2025, while average applications per role jumped 26%. https://fortune.com/2026/03/18/blackrock-ceo-larry-fink-class-of-2026-gen-z-college-graduate-warning-ai-job-market-crisis-unprepared-workforce-skilled-trade-growth/ ↩

- Kickresume survey, 2025: 58% of Gen Z graduates from the classes of 2024 and 2025 were still searching for their first job, compared to 25% of millennial and Gen X graduates in previous years. Cited in Fortune, March 17, 2026. https://fortune.com/2026/03/17/servicenow-ceo-bill-mcdermott-gen-z-graduates-face-30-unemployment-next-couple-of-years-ai-takes-over/ ↩

- In May 2026, Ken Griffin, founder and CEO of hedge fund Citadel Securities, spoke at the Stanford Leadership Forum, reporting that AI was already doing the work of Masters-level and Ph.D.-level employees. The only difference was that AI could do it in hours where traditional employees took weeks or months. ↩

- University at Buffalo School of Law, "Applications & LSAT Scores on the Rise" (August 14, 2025): "An 18% increase in applicants and a 22% increase in applications, according to data provided from the Law School Admission Council (LSAC), represents the highest volume of law school applicants in over a decade." https://www.law.buffalo.edu/blog/2025-law-admissions-trends.html ↩

- LSAC, "Too Soon for Predictions, but the 2026 Admission Cycle Is Starting Strong" (October 2025): "the total number of applicants is currently up 33 percent." https://www.lsac.org/blog/too-soon-predictions-2026-admission-cycle-starting-strong; see also Legal.io: https://www.legal.io/articles/5745904/Law-School-Applications-Surge-33-Intensifying-Competition-for-2026-Admissions ↩

- LSAC blog (October 2025): "The August LSAT administration had approximately 26,000 test takers, up 18 percent compared to the same administration last year…September saw approximately 23,000 test takers, an increase of 24 percent over last year. The October administration…had approximately 26,000 test takers, up 16 percent from last year." https://www.lsac.org/blog/too-soon-predictions-2026-admission-cycle-starting-strong ↩

- Legal.io, "Law School Applications Surge 33%" (October 2025), quoting Mike Spivey: "In my 26 years of staring at the [council's] volume summary report, I've never seen a cycle starting this much up." https://www.legal.io/articles/5745904/Law-School-Applications-Surge-33-Intensifying-Competition-for-2026-Admissions ↩

- Martin, Iain, and Anna Tong. "Legal AI Startup Legora Eyes $400 Million Raise At $5 Billion-Plus Valuation." Forbes, February 17, 2026. https://www.forbes.com/sites/iainmartin/2026/02/17/legal-ai-startup-legora-eyes-400-million-raise-at-5-billion-plus-valuation/ ↩

- "Legora Announces $550M Series D at $5.55B Valuation," Legaltech News, March 10, 2026. https://www.law.com/legaltechnews/2026/03/10/legora-announces-550m-series-d-at-555b-valuation-/ ↩

- "Anthropic launches Claude for Legal, giving lawyers 20 new program integrations and 12 practice area plugins," ABA Journal. https://www.abajournal.com/news/article/anthropic-launches-claude-for-legal-giving-lawyers-20-new-program-integrations-and-12-practice-area-plugins ↩

- MBA application decline data at less selective programs from Graduate Management Admission Council (GMAC) and widely reported in higher education media in 2025. ↩

- PBS NewsHour / Associated Press, "Melania Trump shares the spotlight with a robot at an education and technology event" (March 26, 2026): First Lady Melania Trump appeared alongside Figure AI's humanoid robot Figure 03 at the "Fostering the Future Together Global Coalition Summit" in the White House East Room. Trump proposed a hypothetical humanoid educator named "Plato" that would deliver personalized instruction in classical studies, science, and mathematics "in the comfort of your home." Education Secretary Linda McMahon attended from the front row. AFT President Randi Weingarten called the proposal "every parent's nightmare." https://www.pbs.org/newshour/politics/melania-trump-shares-the-spotlight-with-a-robot-at-an-education-and-technology-event. See also NBC News, "Teachers union boss blasts Melania Trump's robot pitch: 'Every parent's nightmare'" (March 27, 2026). https://www.nbcnews.com/tech/tech-news/melania-trump-robot-video-union-teacher-education-rcna265297 ↩

- Anthropic, "Introducing Claude for Education" (April 2, 2025): announcement of Claude for Education, including campus-wide partnerships with Northeastern University (50,000 students and faculty across 13 global campuses, designated Anthropic's first university design partner), London School of Economics, and Champlain College; partnerships with Internet2 and Instructure (Canvas LMS); and the introduction of "Learning Mode," a Socratic feature that guides student reasoning rather than providing direct answers. https://www.anthropic.com/news/introducing-claude-for-education ↩

- Trump FY2026 budget proposals for NIH and NSF cuts widely reported. The 40% (NIH) and 57% (NSF) cumulative reduction figures since FY2024 are from federal budget analysis. ↩

- Federal grant terminations ($3.3–3.7B) targeting universities, affecting land-grant institutions and HBCUs, from 2025 reporting on federal research funding cuts. ↩

- Bryan Alexander, "Academic closures, mergers, and cuts: heading into fall 2025" (August 31, 2025): University of Chicago PhD admissions pauses across humanities and social science departments. https://bryanalexander.org/horizon-scanning/academic-closures-mergers-and-cuts-heading-into-fall-2025/ ↩

- Bryan Alexander, "Campus cuts, closures, mergers, and layoffs for winter 2025–2026" (February 2026): "University of Texas at Austin is closing its American Studies department along with several gender and ethnic studies and language departments." https://bryanalexander.org/horizon-scanning/campus-cuts-closures-mergers-and-layoffs-for-winter-2025-2026/ ↩

- The Earnings Premium requires programs to fail the threshold in two of three consecutive years before losing Direct Loan eligibility, with first calculations due July 2027. The earliest effective date for loss of eligibility is July 1, 2028. Pell Grant eligibility is not affected by the EP. These details matter for regulatory analysis but the practical effect — students at vulnerable institutions losing the ability to borrow — was immediate and severe once the threshold began binding. ↩

- Amodei's warnings were extensive and escalating. In May 2025, he told Axios that AI could eliminate half of all entry-level white-collar jobs and push unemployment to 10–20% within five years. In September 2025, he told an Axios summit that the technology was "moving very quickly" and that Anthropic "felt there was a need to warn the world." In January 2026, he published a roughly 20,000-word essay arguing the risks were not being taken seriously and warning of an "unusually painful" labor market shock, calling for government intervention including progressive taxation of AI firms. See: https://www.axios.com/2025/05/28/ai-jobs-white-collar-unemployment-anthropic; https://www.cnn.com/2025/09/17/business/anthropic-warns-ai-could-soon-replace-jobs; https://www.cnbc.com/2026/01/27/dario-amodei-warns-ai-cause-unusually-painful-disruption-jobs.html ↩

- Altman funded the largest basic income study in U.S. history through his nonprofit OpenResearch, providing $1,000/month to 3,000 low-income participants in Illinois and Texas for three years (results published 2024). By August 2025, he had moved beyond traditional UBI to advocate for "universal extreme wealth," proposing that a share of global AI output be distributed to all citizens. See: https://qz.com/sam-altman-openai-free-money-basic-income-study-1851600997; https://finance.yahoo.com/news/sam-altman-wants-universal-extreme-124300850.html ↩

- Higher Education Inquirer, "A Preliminary List of Private Colleges in Trouble" (August 2025): "Siena Heights University in Adrian, Michigan, will close after the 2025–2026 academic year. Founded in 1919, the Catholic university has seen enrollment drop by nearly a third in the past decade." https://www.highereducationinquirer.org/2025/08/a-preliminary-list-of-private-colleges.html ↩

- University Business, "Labouré College of Healthcare is latest to close in 2026" (March 2026): Lourdes University closure details, board describing operating model as "no longer…sustained." https://universitybusiness.com/the-college-closings-and-mergers-of-2026/ ↩

- University Business (2026 closures tracker): "Clarks Summit University announced its closure leading up to the fall semester on July 1 after 'hav[ing] exhausted every viable solution to bridge a significant financial gap.'" https://universitybusiness.com/the-college-closings-and-mergers-of-2026/ ↩

- The policy architecture had been previewed years earlier. OpenAI's April 2026 white paper, "Industrial Policy for the Intelligence Age: Ideas to Keep People First," proposed thirteen major policy interventions including retraining vouchers, portable benefits, adaptive safety nets, and expanded community college funding. Not one was directed at sustaining four-year colleges or universities. https://openai.com/index/industrial-policy-for-the-intelligence-age/ ↩

- Fortune, March 17, 2026: ServiceNow CEO Bill McDermott predicted new college graduate unemployment could reach "the mid-30s in the next couple of years," citing the displacement of entry-level roles by AI agents. https://fortune.com/2026/03/17/servicenow-ceo-bill-mcdermott-gen-z-graduates-face-30-unemployment-next-couple-of-years-ai-takes-over/ ↩